Disclaimer: I had previously bought Apogee Enterprises on 21 June 2024 and sold it on 4 Oct 2024. I was due to write this analysis whilst I still owned some shares but as the price appreciated faster than I anticipated and within my valuation range, I decided to sell. That goes without saying, I still think the company is of investment quality.

Why I Like APOG

- Demonstrated growth over the past decade

- New CEO and new strategic direction have overachieved some of the financial targets.

- A well-known value investor sits on the board

- Low P/E, High Return on Capital

- Undervalued compared to peers

Company Background

Apogee Enterprises (APOG) is a Minneapolis based company that provides architectural products and services for enclosing buildings, and high-performance glass and acrylic products used in applications for preservation, protection and enhanced viewing. In simpler terms, its designs and manufactures glass for buildings.

The company operates through four segments: Architectural Glass, Architectural Services, Architectural Framing Systems and Large-Scale Optical Technologies (LSO).

It caters to the US, Canada and Brazil; and has a market cap of about USD 1.8bn at the time of writing this post.

Growth Track Record

APOG has a solid track record of growth. As of FY 2024, it generated revenues of USD 1.4bn which had gradually increased over the past 10 years. It is profitable and margins have been improving as of recent. It is free cash flow positive generating USD 161m by FY2024 (up from USD 45m in 2015). In terms of its solvency, risk seems to be manageable supported by solid and improving credit metrics: Debt/EBITDA improved to 0.4x in 2024 having peaked at 2.4x in 2022.

Snapshot of financials:

In short, APOG is in good shape.

New CEO, New Focus

In 2021, APOG appointed a new CEO (Ty Silberhorn) who shifted the strategic focus of the company from less profitable business segments to more profitable ones. In August of the same year, he announced restructuring and cost reduction plans in the face of a challenging environment (global supply chain disruption being prominent). In Nov 2021, APOG set three-year financial targets for return on invested capital (ROIC), operating margin, and revenue growth. So far, the first two financial targets have been achieved.

- Return on Invested Capital (ROIC) greater than 12% (FY2024: 16.5%)

- Operating margin greater than 10% (FY2024: 10.3%)

- Revenue growth greater than 1.2 times the overall non-residential construction market (not yet achieved)

To add to the above, the company had announced “Project Fortify” in Jan 2024 “to further streamline its business operations, enable a more efficient cost model, and better position the Company for profitable growth”.

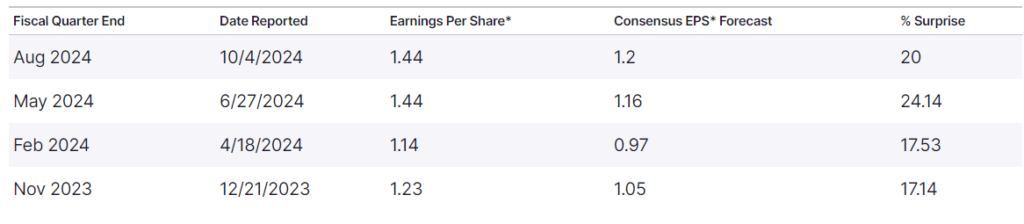

APOG had beat earnings multiple times and EPS improved quite a bit in the last 2 years. EPS now stands at USD 4.7, up from USD 2.3 in 2020.

Source: www.Nasdaq.com

A Well Renowned Value Investor Sits on The Board

Just as assessing management is crucial, it’s equally important to evaluate the board members. One name on the board that I recognized and found particularly noteworthy is Elizabeth Tilly, Chief Investment Officer and Executive Vice President of The Pohlad Companies.

Tilly was a featured guest on the podcast Value Investing with Legends. Among the many insightful perspectives she shared, I recall something she said that is particularly important why she sits on APOG’s board.

When the interviewer asked about her approach to questioning managers, Tilly explained that she often tries to determine whether the managers (i.e., CEOs) can realistically meet their targets or KPIs. If they seem capable, she then pushes them to aim for even higher targets.

So why is this important to APOG?

- First of all, APOG has not only managed to achieve 2 of its 3 targets earlier than expected but has also significantly exceeded its ROIC target. To me, it seems that APOG had a lot of onset inefficiencies that were easy to get out of the way…and very fast.

- Second, if most of the easy fixes are out of the way, that means that management has more room to explore further. With the right direction, creativity and push, they can further enhance their performance efficiency.

- Finally, whilst we all know that public companies do seem to have ambitious targets that they share with the public, they rarely set out difficult targets that would jeopardize the company’s view publicly.

Therefore, with Elizabeth Tilly on board, I’m sure that she has adopted the same style of questioning and is pushing APOG’s CEO to achieve even higher goals. This could only mean a higher future value for APOG.

Low P/E, High Return on Capital

When I started looking into APOG, it was trading at about 10x P/E. Historically, APOG’s normalized P/E ranged between 13x to 33x since 2014. So compared to its history, there is only way one that value can go with higher expected earnings.

Additionally, with the shift in focus, APOG’s return on capital is around 38% which is reasonably healthy. A high return on capital does not only mean that a company is converting more profits using less resources, it also means that it could potentially have a competitive advantage compared to its competitors.

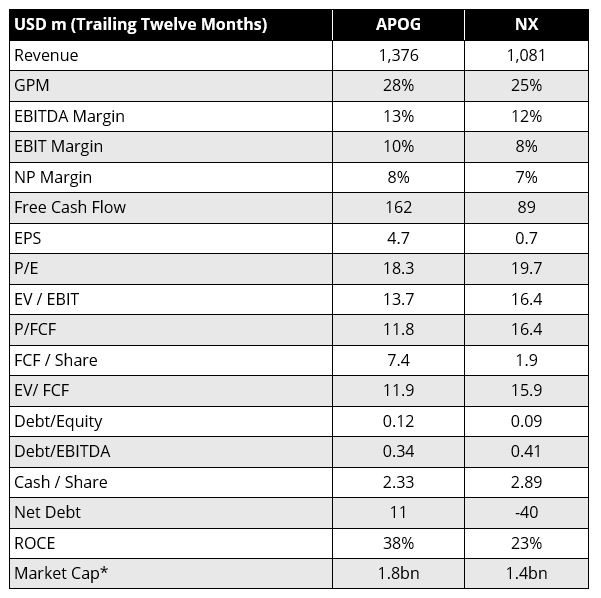

Comparing to Peers

I’ve selected one competitor, Quanex Building Products Corporation (NX), to compare against APOG. APOG is clearly a better investment with higher profit margin and return on capital employed (ROCE). It generates more revenue, profit and free cash flow. In addition, every valuation multiple is comparably smaller than NX’s, indicating that APOG should be valued higher.

* During my purchase period, the market cap of APOG was lower or on par with NX.

Valuation

In July 2024, at the time when APOG’s market cap was about USD1.4bn, I valued APOG at USD1.8bn, conservatively. This was based on DCF valuation as well as multiple based approach. If APOG manages to turnaround revenue growth and also achieve its 3rd financial target, then I foresee APOG growing in value, possibly to the USD 2.5bn-3.0bn range.

Conclusion

Being a student of the Warren Buffett School of Investing, one should always ask: If the stock market ended up closing tomorrow, would I still invest in the company? The answer is a resounding Yes.

Therefore, APOG is a buy in my books.