When you think AI, you think tech. You don’t think cooling.

- A beneficiary of AI infrastructure growth via data centre cooling demand

- Explosive Revenue, EPS and Free Cash Flow growth since 2022

- Technology sector revenues grew from 13% to 45% of total

- Record backlog of $11.9bn (FY2025) and strong growth provide strong revenue visibility

- Strong Liquidity: Negative net debt and $921m undrawn credit facility

- Well diversified across sectors, not just AI data centres

The Investment Case

There is little doubt that AI is on a sustained growth trajectory, having already become deeply embedded in our daily lives, both commercially and personally, whether through direct use or through technologies operating in the background. To be part of this value wave, you can either 1) invest directly in AI (companies like Google or, if it were public, OpenAI) or 2) take an indirect route through the infrastructure that makes AI physically possible.

That indirect route is where I found Comfort Systems USA, a HVAC company based in Delaware, USA.

How Does an HVAC Company Benefit from AI Growth?

AI growth goes hand-in-hand with data centre growth. Data centres are required to process and store enormous volumes of data for AI purposes. In turn, data centres consume large amounts of energy producing lots of heat. Cooling is therefore not optional; it is existential to keep these data centers running, and even more so for AI data centres as they utilize much more energy than normal.

My initial instinct was to look at water utility companies, since water is the primary cooling medium for most large infrastructure. However, utility companies are heavily regulated, geographically limited, and slow growing; which offers little upside or meaningful exposure to the pace of AI growth.

That led me to explore HVAC systems as an alternative. Companies like Comfort Systems USA specialize in designing, installing, and maintaining these systems, providing an alternative and scalable way to invest in the physical infrastructure behind AI, without the constraints of the utilities sector.

About The Company

Comfort Systems USA ($FIX) is a heating, ventilation, and air conditioning (HVAC) company headquartered in Delaware, USA. It operates through two segments, Mechanical and Electrical, and maintains a nationwide footprint across 190 locations in the United States, supported by more than 22,000 employees. $FIX also pursues a disciplined acquisition strategy, deploying a significant portion of its cash flows on acquisitions that have consistently driven revenue growth and margin expansion.

The company’s core service lines include:

- Mechanical Services: HVAC system design, installation, and maintenance

- Plumbing and Piping: Comprehensive plumbing solutions and process piping

- Electrical Services: Electrical system installation and servicing

- Modular Construction: Off-site construction solutions for HVAC, electrical, and data centre modules

- Building Automation: Turnkey solutions for life safety systems, remote monitoring, and system operations

A Decade of Compounding

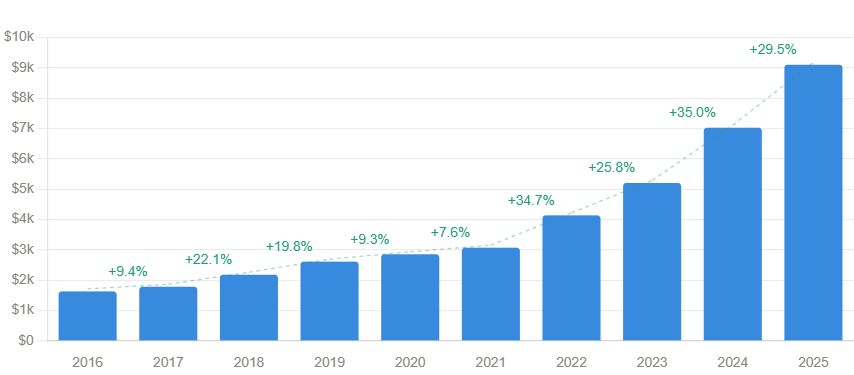

Revenue Growth

In FY2025, revenues reached a peak of USD 9.1 billion having grown outstandingly in recent years: +35% in 2022, +26% in 2023, +35% in 2024, and +30% in 2025. Clearly, $FIX’s performance is not the result of a single strong year, but reflects sustained momentum supported by consistent double digit growth.

Revenue Breakdown by Sector

While Comfort Systems does not segregate data centre revenue explicitly, it does segment revenue by sectors. The Technology segment, which includes data centres and chip manufacturing, tells a compelling story on its own (see below table). Revenues from Technology segment has grown from 13% of revenues in 2022 to 45% in 2025, with the sharpest acceleration occurring in the last two years, in line with the AI boom. The remaining revenue base across manufacturing, healthcare, and education provides meaningful diversification.

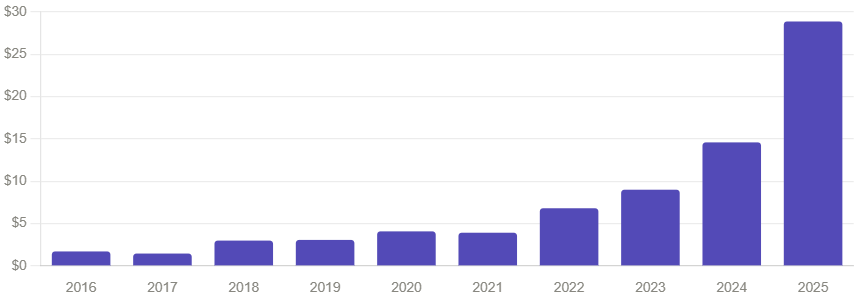

Earnings Per Share

EPS for FY2025 came in at USD 28.9, nearly double that of the prior year, demonstrating strong profitability.

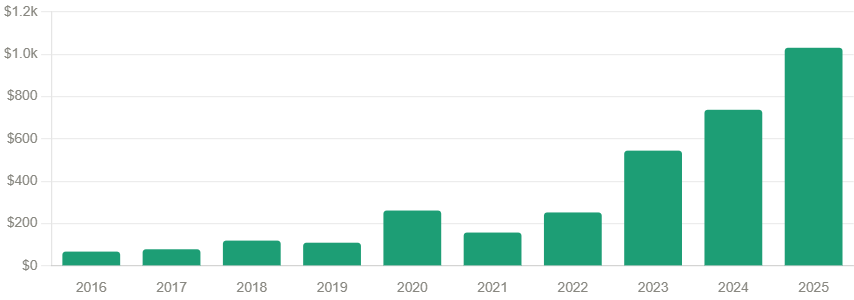

Free Cash Flow

Free Cash Flow flow grew to USD 1.0 billion in FY2025 (highest to date), tracking closely with operating cash flows as net income compounded from USD 246 million in 2022 to USD 522 million in 2024. The business is highly cash generative, which funds both its acquisition strategy and its balance sheet strength.

What Makes $FIX Resilient

Negative Net Debt

As of FY2025, Comfort Systems reported negative net debt of USD 196 million. In other words, it can pay off all its outstanding debt using cash and still have some left; even after taking on USD 112 million in additional bank loans during the year. The company also has USD 921 million of undrawn RCF, demonstrating good liquidity.

Record Backlog

Backlog as of FY2025 reached USD 11.9 billion, having doubled from 2024. On a same-store basis (excluding new acquisitions), backlog had grown from USD 6 billion to USD 11.6 billion, which means it is winning contracts faster than it can deliver existing ones. With strong backlog, revenue is locked in for the foreseeable future.

Well Diversified Even Without AI

Even if AI investments slows materially for whatever reason, Comfort Systems would still operate a significant business across manufacturing, healthcare, education, and other sectors. This diversified sectorial exposure provides limited downside risk in terms of revenues and operational performance. AI data centres were responsible for most of the growth in the last few years but do not represent the whole business.20

Risks to Consider

AI Capex Slowdown

The single biggest risk is a pullback in data centre construction spending by the major cloud and AI players (Microsoft, Google, Amazon, and Meta). These companies effectively dictate market sentiment and movement when it comes to AI expansion. Any signal of capex discipline could negatively new contract wins and backlog growth.

Tariff and Materials Cost Exposure

HVAC installations are materials intensive, relying on copper, steel, and aluminium, all of which are exposed to tariff risk in the current trade environment. This could increase input costs and squeeze margins if not passed through to customers.

Execution Risk from Acquisitions

Comfort Systems has grown partly through acquisitions. While this strategy has been well executed historically, a poorly integrated acquisition could drag on margins or divert management attention at a critical growth juncture.

Valuation

I apply value investing principles when assessing intrinsic value, using a discounted cash flow framework with a proprietary discount rate set above the prevailing treasury rate. Rather than relying on WACC, I use a conservatively calibrated hurdle rate that reflects the risk I am willing to accept.

For $FIX, I forecast free cash flow growing at 15% per year — a deliberately conservative assumption relative to the company’s 5-year CAGR of 60% and 10-year CAGR of 35%. Based on this model, I estimate the intrinsic value of $FIX at approximately USD 1,990 per share.

Applying my standard 50% margin of safety, I would be a buyer at any price below USD 990. At current levels, the stock is a great business but not yet a screaming bargain. I would wait for a meaningful market correction before getting in.

For context: I am already a shareholder. I took my initial position during the DeepSeek driven sell off in early 2025, when the market indiscriminately punished AI related companies on fears that cheaper AI models would reduce infrastructure demand.